Claims

Failure to adhere to this guide in conjunction with the Policy may have serious effects on your rights to receive benefits. Violations of the provision in either document may result in Claim adjustments, Claim denials, or a rescission of coverage.

Filing a Claim

LGIS has simplified the process of filing a Claim. It starts with a simple written or electronic request for benefits as displayed in the Claim form. Upon receipt of the request, your Claim is assigned to a claim specialist with LGIS (“Claim Specialist”) who will work to process your Claim and perfect such Claim in a timely manner. A Claim is considered “perfected” when we have received all information needed to process it. This information includes documentation as well as access to the property. We make every effort to request any additional information needed over the phone. However, sometimes we need written documentation to perfect your Claim so it may be settled. In these cases, your Claim Specialist will request the information within twenty (20) days of receipt of the Claim.

Please include a copy of the payment history for the Loan as well as copies of any values obtained to expedite processing of your Claim. See Section 6.0 – FAQ's & Forms – Claim Processes for additional documentation and information that may be requested to process your Claim.

FAQs

When to File a Claim

You should file your Claim within sixty (60) days of acquiring the Borrower’s title to the property or within sixty (60) days of the closing of a pre-approved property sale. In states where there is a post-sale redemption period, you may file the Claim within sixty (60) days of expiration of the redemption rights. Failure to file a Claim within the time frames stated may extinguish your rights to benefits under the Policy.

How to File a Claim

Electronic Filing

We accept both electronic and manual Claim filings. If you are not currently set up to submit your Claim to LGIS electronically, you may contact the Loss Management Department. You may also submit your Claim through the Internet via (LGIS proprietary software – yet to be developed.) You will need a username and password for access.

Non-Electronic Filing

You may file a Claim by completing LGIS’s Claim form or any mutually agreed upon format. LGIS’s form may be found in Section 6.0 – FAQ's & Forms.

Read MoreFAQs

Claimable Items

Calculations of a Claim typically consists of the expenses listed below. This list includes items allowed under the Policy and items associated with the foreclosure process. Any inconsistency yielding to the Policy. Section 4.5 for line items instructions on the Claim:

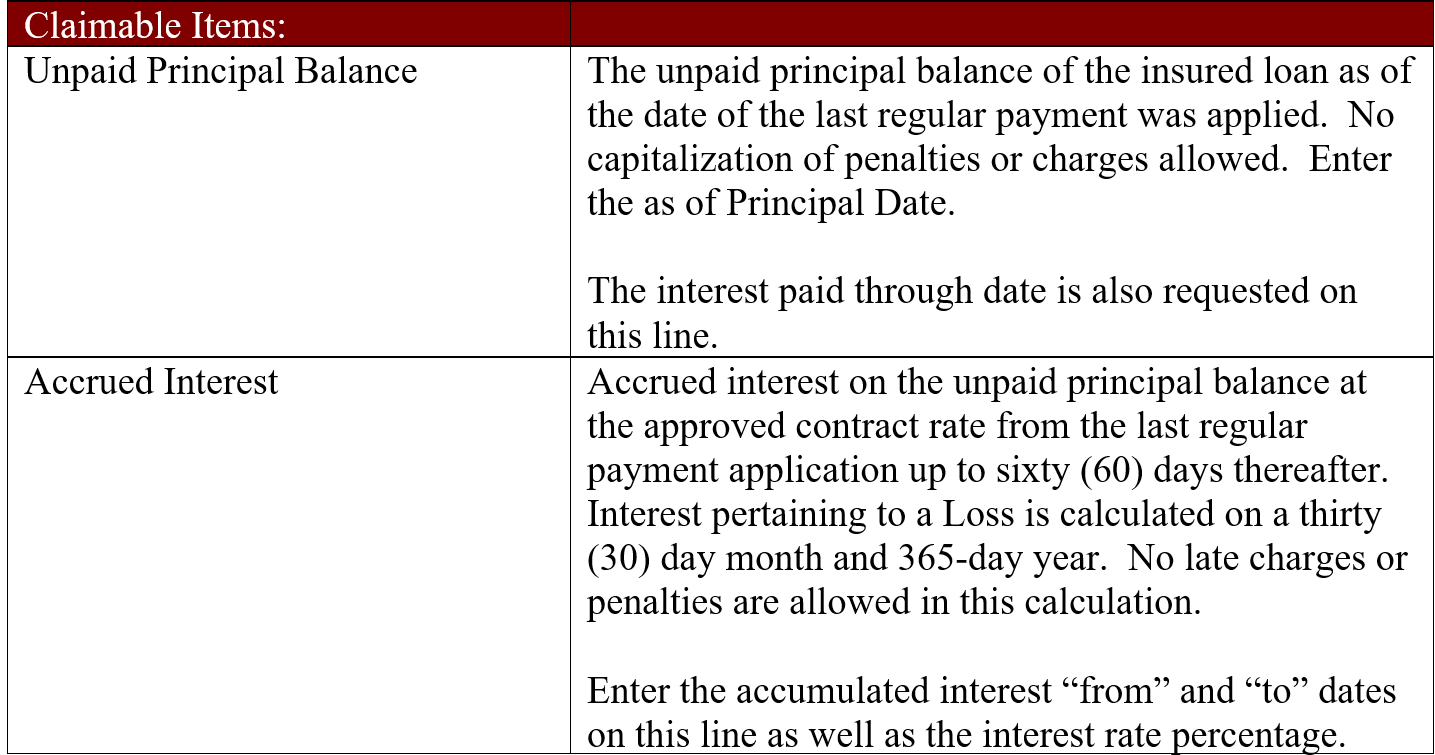

- The amortized unpaid principal balance of the insured loan as of the date the last regular payment was applied. No capitalization of penalties, accrued interest or charges is allowed.

- Accrued interest on the unpaid principal balance at the approved contract rate from the last regular payment application for a maximum of sixty (60) days. No late charges or penalties are allowed in this calculation.

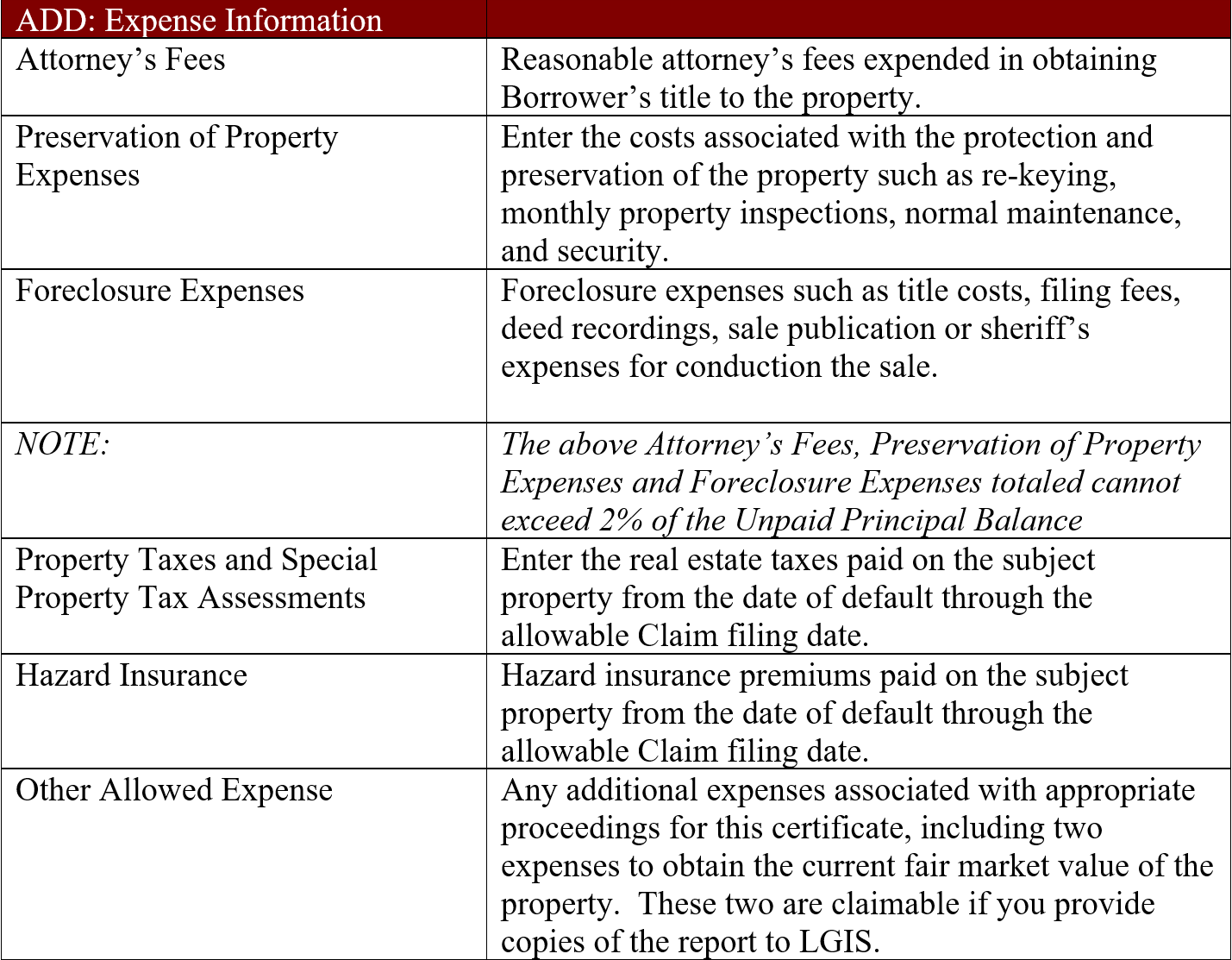

- Reasonable:

- Attorney's fees expended on obtaining the Borrower's title to the property.

- Property preservation costs to protect the property from damage such as re-keying, monthly property inspections, normal maintenance and security.

- Foreclosure Expenses such as title costs, filing fees, deed recordings, sale publication or sheriff's expenses for conduction the sale.

- The above fees are limited to 2% of the unpaid principal balance.

- Property Taxes and Special Assessment – to be included in Claim, property taxes and any amounts paid toward special assessment shall have been advanced from the Insured’s funds and shall be pro-rated to the date of the foreclosure sale, or date the property is sold for a maximum of two (2) months from default and included in the Property Preservation Allowance.

- From escrowed accounts, real estate property taxes are prorated from the date of default to the allowable Claim filing date. Same with any special property tax assessment.

- From escrowed account, hazard insurance premium is prorated from the date of default to the allowable Claim filing date and included in the Property Preservation Allowance.

- Other Allowed Expenses:

- Two expenses incurred to obtain the current fair market value of the property are claimable if you provide copies of the reports to LGIS when requested.

- Any other miscellaneous expenses approved in writing by LGIS.

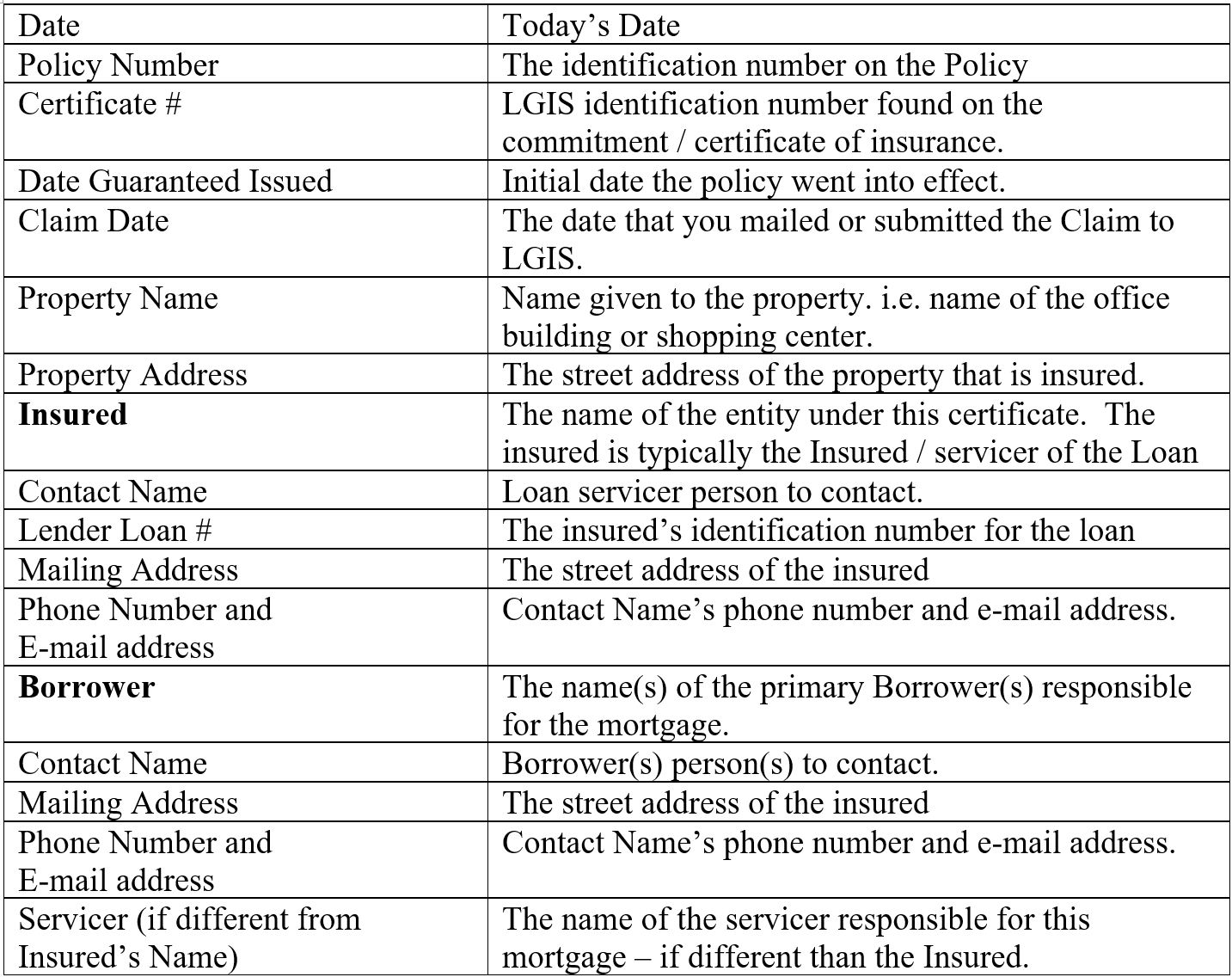

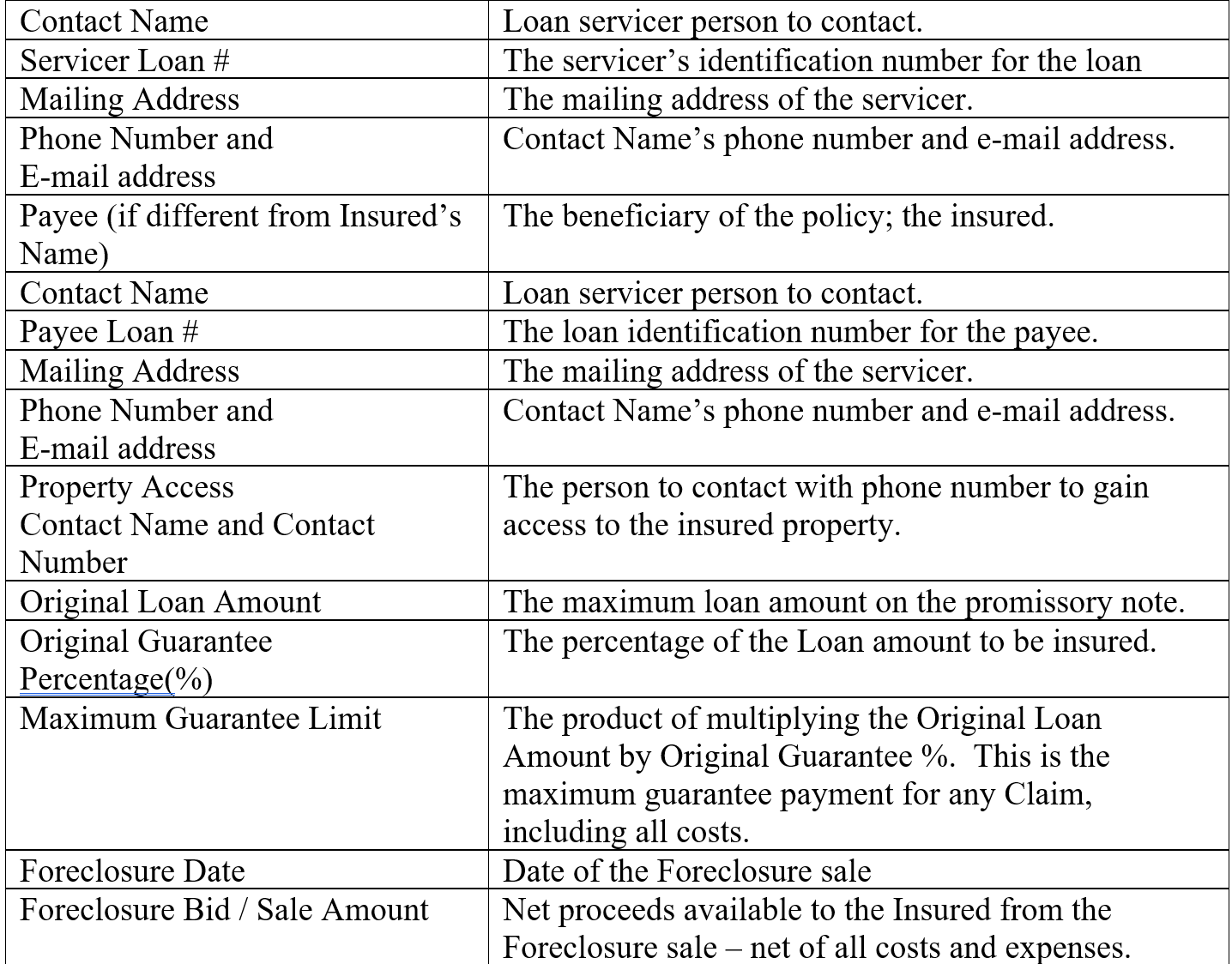

Line Item Instructions for a Claim for Loss

Claim form terminology is listed below to assist you in completing your form.

Claimable Items Table

Expense Information Table

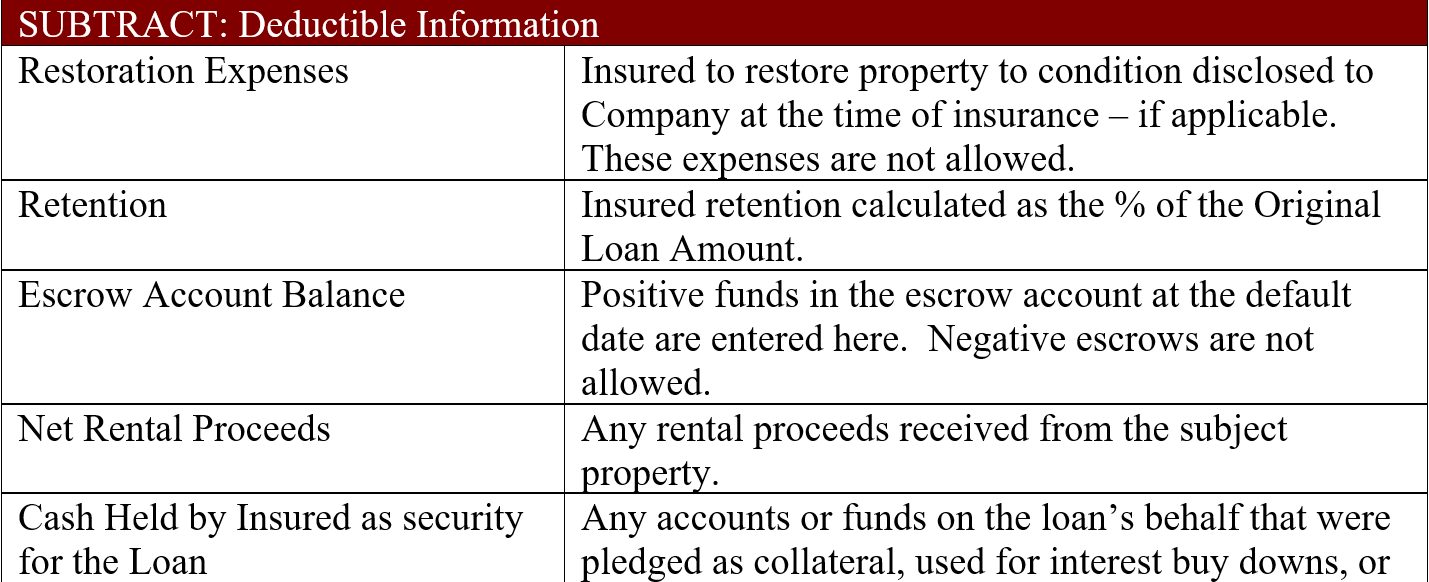

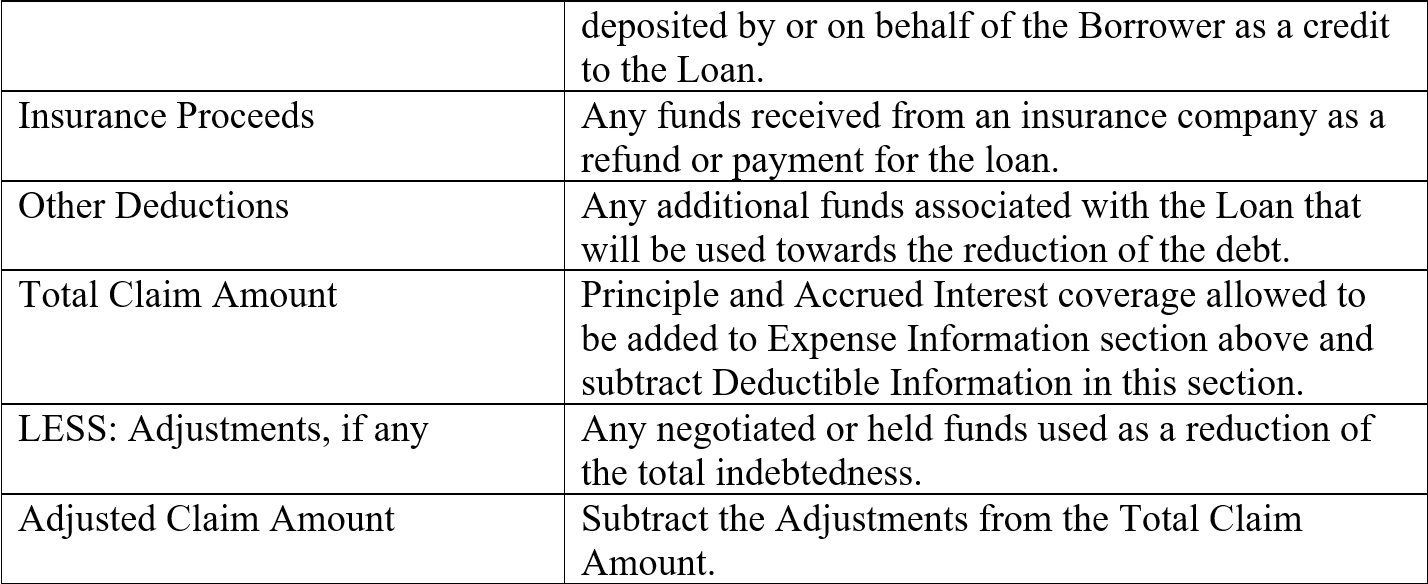

Deductible Information Table

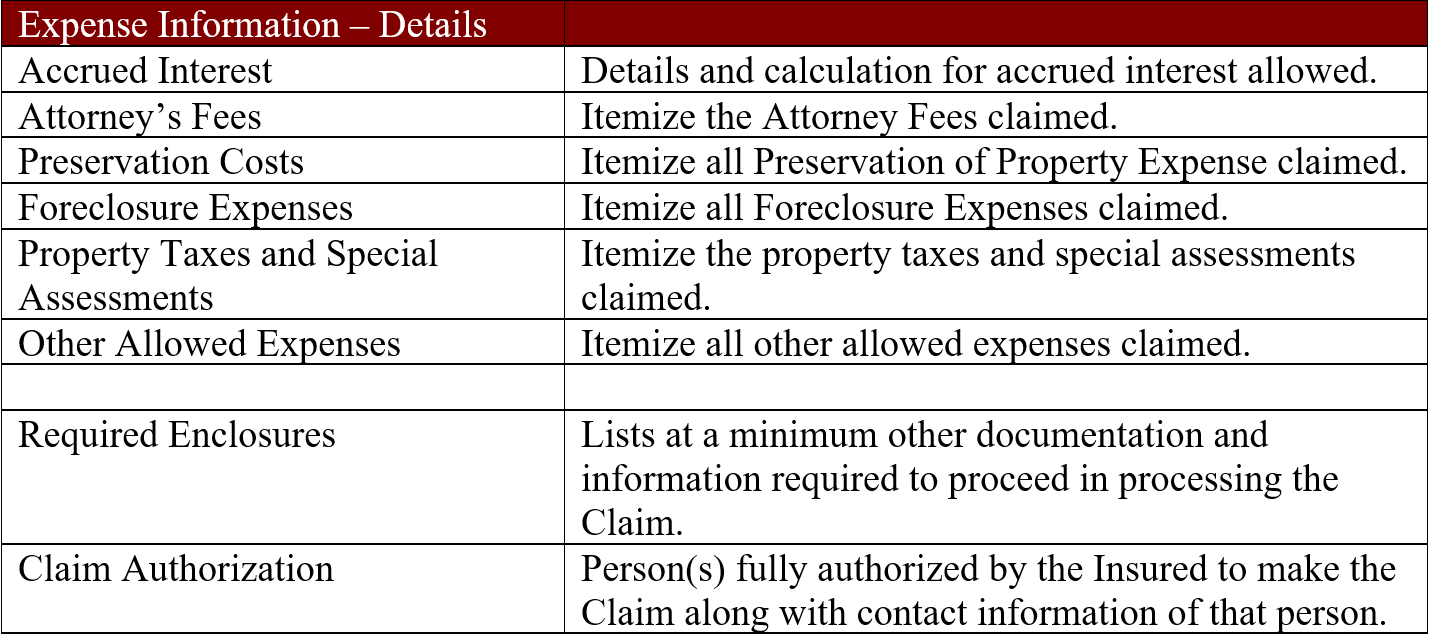

Expense Information – Details

Non-Claimable Items

Do not list items on the Claim form that are not claimable under the Policy. The list below includes typical, but not all, items that are not claimable:

- Extended interest for unreasonable delays in the foreclosure process.

- Delinquent real estate property taxes or liens due before the date of default (unless you obtain prior written approval from LGIS).

- Judgments or liens placed against the property.

- Late charges or penalties imposed on the Loan.

- Late charges or liens from property associations.

- Tax penalties.

- Inspection photos.

Deductible Items on the Claim

There are many items associated with a Loan that will be deducted from the Claim calculation. This list is typical of what we see submitted in the Claim that are not claimable and disallowed from the calculation when processing your Claim. This list is not inclusive of all non-claimable items:

- The positive balance in the escrow account as of the date the last regular payment was applied.

- Buy down funds or other compensating balances pledged on the loan.

- Rental or other income collected from the property.

- Hazard insurance refunds.

- Suspense or holding account funds.

- Borrower contributions or partial payment.

- Net proceeds amount from the sale of the property.

- Restoration of the property.

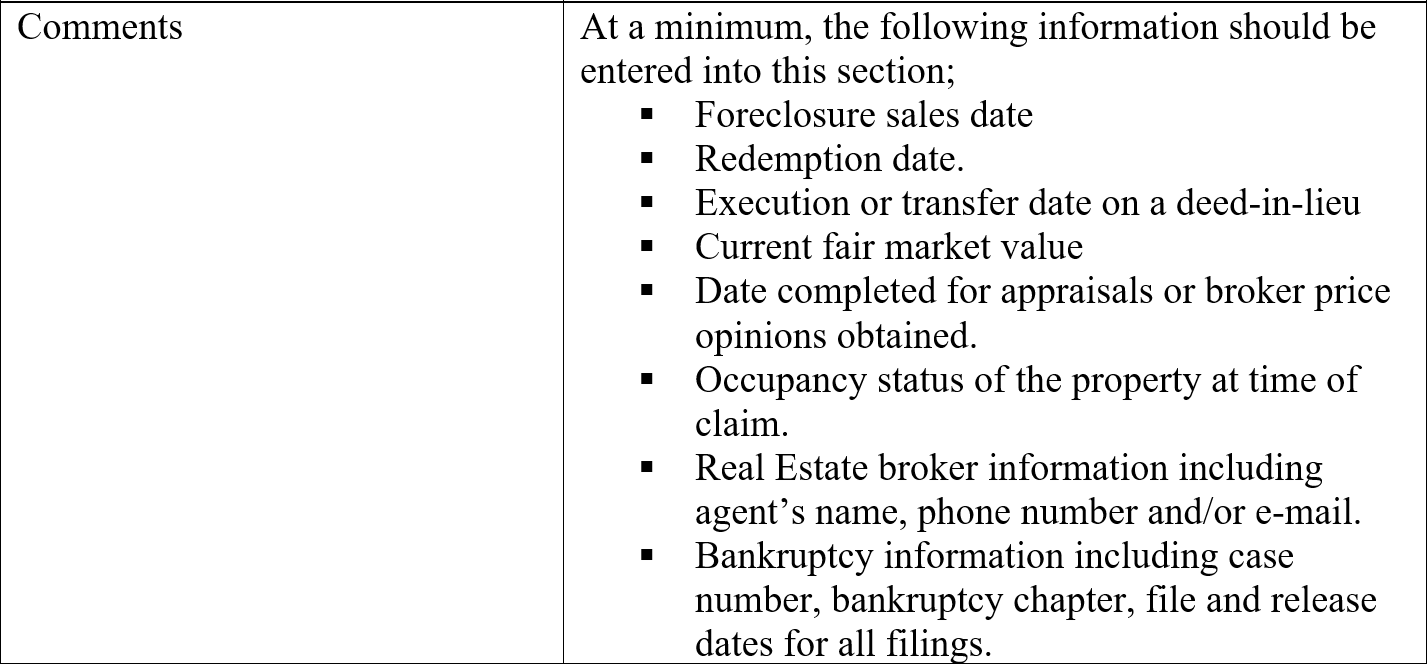

Comments Section of the Claim

To expedite the processing of your Claim please include the following information in this section:

- Foreclosure sales date.

- Redemption date.

- Execution or transfer date on a deed-in-lieu.

- Current fair market value.

- Date completed for appraisals or broker price opinions obtained.

- Occupancy status of the property at time of Claim.

- Real Estate broker information including agent’s name, phone number and/or e-mail.

- Bankruptcy information including case number, bankruptcy chapter, file and release dates for all filings.

Claims Settled Without Payment

There are times when a Claim request is closed, and the coverage cancelled without payment. This typically happens when you receive make whole funds prior to settlement of the Claim, if you fail to provide LGIS with all requested information to complete the processing of your Claim after three written attempts to obtain the information and more than sixty (60) days have elapsed since the last request, or if you are outside of the one hundred-eighty (180) or two hundred-forty (240) day allowance for providing requested information, whichever shall occur first.

Where Payment Is Made

Upon validation, Claim settlements are sent to the verified payee named on the Claim form. This is typically the servicer of the loan that is also listed on the Claim form.

Exclusions from Coverage

As discussed in the Exclusions section of your Policy, several situations may affect your benefits. Please refer to your Policy for a complete listing.

Normal wear and tear to the property is not considered physical damage and will be reviewed upon receipt of the Claim. Physical damage more than $1,500 requires the restoration of the property to its original condition as of the date of insurance or that an adjustment be made for net harm caused to LGIS as a result of the damage.

Explanation of Benefits (EOB)

To assist you with understanding the Claim settlement amount that you receive, we provide an explanation of benefits letter. The letter includes the following information:

- The expenses you filed in your request.

- The expenses we allowed in your settlement.

- Reasons certain expenses were disallowed or adjusted.

- Vital information on when, how and who we paid.

Supplemental Claims

The settlement of a Claim is considered the full and final discharge of our obligations under the Policy. Therefore, it is imperative that all Claim information is included prior to settlement since there are no further supplemental Claim after settlement.

Eminent Domain Requirements

In the event that part or all of the property is taken by eminent domain or other proceedings by a federal, state or local governmental unit or agency. LGIS requires that all maximum permissible amounts of compensation awarded be applied to reduce the unpaid and insured principal balance of the Loan in accordance with the law of the jurisdiction where the property is located.